B2B Software Market Trends, May 2026: Valuations Stabilize & AI Breaks Records

Market Update

B2B Software Market Trends, May 2026: Valuations Stabilize & AI Breaks Records

Dedale Intelligence's B2B software market update for May 2026, covering valuation stabilisation, AI investment acceleration, data and intelligence deal activity, key M&A transactions, and Q1 2026 earnings themes for PE investors and corporate development teams.

April 2026 brought the first meaningful signs of stabilization in B2B software valuations after a sustained four-month correction. The recovery was uneven, the macro environment remained complicated, and the AI investment market continued to rewrite records. This update from Dedale Intelligence covers the themes that mattered most for investors and corporate development teams in April.

Key takeaways from this edition:

EV/Sales NTM multiples for B2B software stabilized at 4.2x in April, 25% below the start of the year and well below the 10-year average of 6.6x, but the sharpest phase of the correction appears to be over

AI investment in 2026 has already surpassed the full-year 2025 total, reaching $233bn in just four months

In Data and Intelligence, proprietary data is the dividing line: unique datasets transact at 10 to 14x EV/Revenue; undifferentiated data clears at 3 to 6x

Corporate M&A rebounded sharply in Q2 to date, lifted by the Brex (approximately €4bn) and HCSS (approximately €2bn) closes; private equity remains quiet at approximately €0.1bn

13 of 15 companies beat Q1 2026 consensus, but stock reactions split almost evenly, confirming the market rewards forward signal quality over headline beats

Valuations: First Signs of Stabilization After a Sharp Correction

The B2B Software Universe, a Dedale Intelligence index of 258 listed companies, gained 5.5% in April 2026, in line with the wider market recovery as the S&P 500 rose 10.4% and the Nasdaq surged 15.3%. The sector remains down 17.9% year-to-date, with ERP/HCM and CRM/CMS the weakest performers at -28% and -31% respectively.

EV/Sales NTM: 4.2x, down from 5.6x at start of 2026, below the 10-year average of 6.6x and at the lowest since Q1 2017

EV/EBITDA NTM: 14.9x, below the long-term average of 27.1x

High-growth companies (above 20%): 7.3x EV/Sales vs. 3.0x for low-growth

Revenue growth premium over FCF margin compressed from 77% in early 2025 to 29% in April 2026

North American software trades at 4.9x vs. 2.7x for European peers, a premium of 81%

For a look at where valuations stood one month prior, see Dedale Intelligence's April 2026 Market Trends

Source: Dedale Intelligence Analysis

Macro: Inflation Spike from the Iran Conflict, Rates Held Steady

Headline CPI jumped to 3.3% in March 2026, up from 2.4% in January and February, driven by a 10.9% spike in energy prices following the Iran conflict. Core CPI remained contained at 2.6%. Both the US Federal Reserve (3.50 to 3.75%) and the ECB (2.00%) held rates unchanged at their April meetings, supporting the valuation stabilization seen in the month.

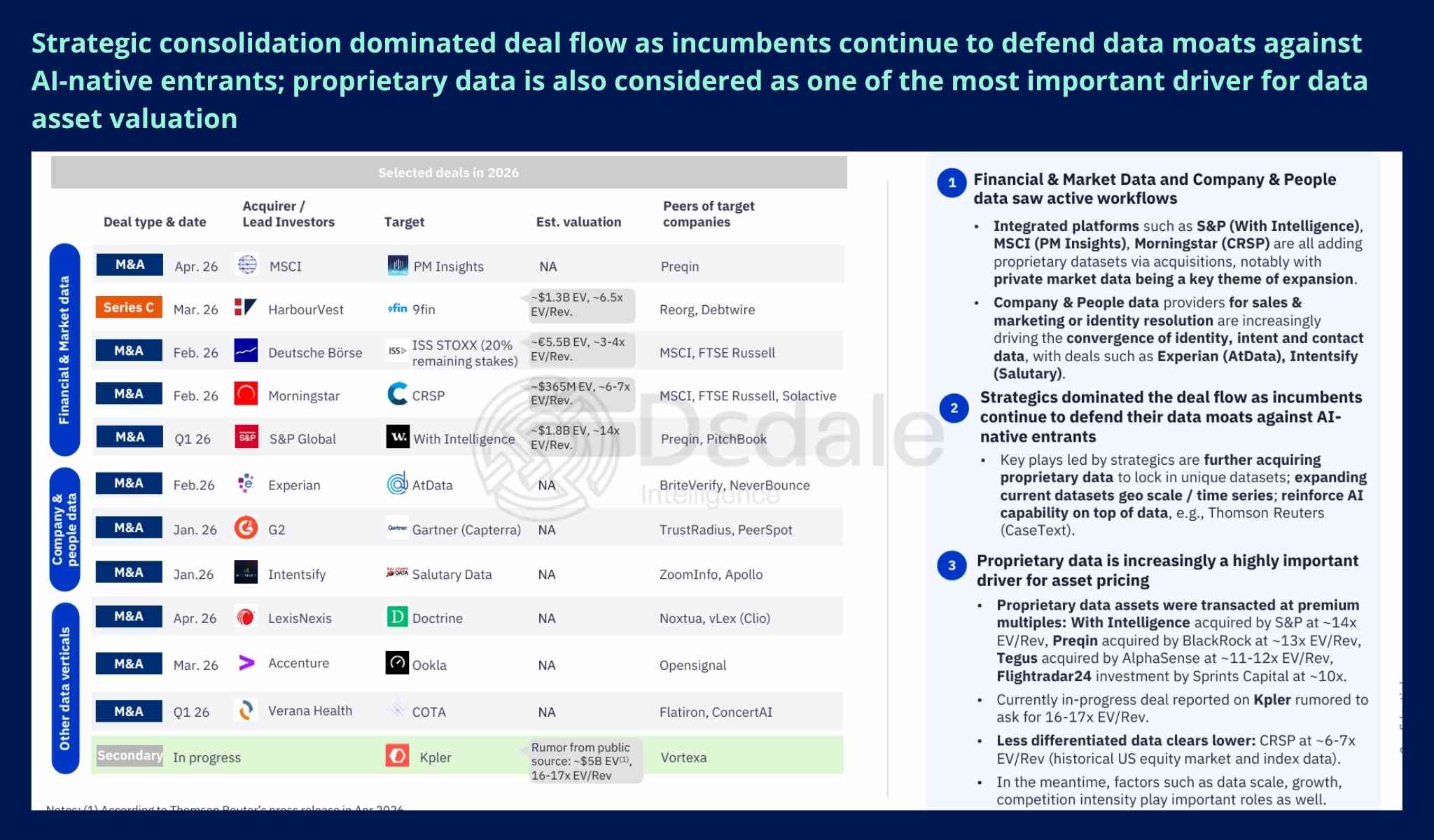

Data and Intelligence: Proprietary Data Creates a Valuation Divide

AI is creating a clear valuation divide in the Data and Intelligence segment. Proprietary data owners, those with unique datasets built through specialist collection, are widening their competitive lead. Aggregators and platforms built on accessible data face growing commoditization risk as AI lowers the barrier to sourcing and structuring similar datasets.

Strategic M&A in 2026 reflects this dynamic, with incumbents acquiring proprietary datasets to defend their moats:

S&P Global acquired With Intelligence at approximately $1.8bn (approximately 14x EV/Revenue)

MSCI acquired PM Insights; Morningstar acquired CRSP at approximately $365m (6 to 7x EV/Revenue)

Experian acquired AtData; Intentsify acquired Salutary Data, converging identity, intent, and contact data

Proprietary assets transacted at 10 to 14x EV/Revenue; less differentiated data cleared at 3 to 6x

From Dedale Intelligence's survey of approximately 100 financial institutions:

64% plan to rationalize or consolidate their data vendor stack over the next three years

Over 60% still expect to retain niche vendors alongside integrated platforms

Integrated platforms showed average budget growth of 9.6% over three years vs. 7.5% for niche providers

For a related view on how data integration and workflow embeddedness drive market dynamics in adjacent segments, see Dedale Intelligence's expert interview on EHS software.

Source: Dedale Intelligence Analysis

The full Data and Intelligence segment analysis, including the complete survey findings and Dedale Intelligence's competitive moat framework, is in the May 2026 Market Intelligence report. Download the full report here.

Deal Activity: Corporate M&A Rebounds, Private Equity Stays Quiet, AI Records Continue

Deal activity in Q2 2026 to date shows a divided market. Private equity remains quiet at approximately €0.1bn across 26 deals. Corporate M&A has rebounded to approximately €10bn, lifted by Capital One's acquisition of Brex (approximately €4bn) and Nemetschek's acquisition of HCSS from Thoma Bravo (approximately €2bn). Other notable April transactions include Amadeus's €1.2bn acquisition of IDEMIA Public Security and Adyen's €750m acquisition of Talon.One at 12.5x EV/Sales.

Venture capital has normalized in Q2 at approximately €10bn across 316 deals, though 2026 YTD AI investment has already reached $233bn, surpassing the full-year 2025 total. April alone saw $23.5bn invested across 125 AI deals. Excluding deals above $500m, the broader market recorded $6.9bn across 122 deals, the most active pace since 2022. The B2B software IPO window remained shut, with zero software listings despite 32 total IPOs across sectors.

Q1 2026 Earnings: Strong Beats, Divided Reactions, Three Structural Themes

The initial Q1 2026 earnings batch covered 15 companies. All 15 reported year-over-year revenue growth, and 13 of 15 beat consensus. Stock performance split almost evenly, confirming the market rewards forward signal quality over headline beats. Three themes stood out:

AI CapEx at scale: Microsoft, Alphabet, Amazon, and Meta are guiding to $125 to $190bn in 2026 CapEx, funding AI infrastructure through headcount reductions. Microsoft's AI business surpassed $37bn ARR (up 120%); Google Cloud accelerated 63% to $20bn.

Middle East conflict creating asymmetric effects: ServiceNow cited approximately 75 basis points of headwind from delayed sovereign deals in the region, while Tenable won a seven-figure deal from a major Middle East financial institution.

Supply chain software bifurcating: SPS Commerce is intentionally churning approximately 4,000 low-revenue Amazon suppliers following a policy change, while Manhattan Associates delivered cloud revenue up 24% with a 70% competitive win rate.

AI Use Case to Watch: Workforce Management for Frontline Industries

Sona Technologies, a UK-based AI workforce management platform founded in 2021 with $102m raised, illustrates the disruption underway in frontline workforce management for social care, hospitality, and retail. Its platform unifies scheduling, attendance, HR, payroll, and communications on a single data layer, with AI handling demand forecasting, shift fill, and payroll compliance. Legacy HCM vendors face a difficult choice between costly retrofitting and acquiring AI-native specialists. Dedale Intelligence is tracking this as one of the HCM sub-segments most exposed to AI disruption.

How Dedale Intelligence Tracks B2B Software Markets

Dedale Intelligence provides monthly B2B software market intelligence for private equity funds, corporate development teams, and M&A advisors across North America and Europe. The analysis in this article is drawn from the May 2026 Market Session. The full report contains detailed valuation tables, deal analysis, earnings summaries, the complete Data and Intelligence deep-dive, and the financial institutions survey results.

%20(1).jpg)