Market Update

Market Trends April 2026

A comprehensive update on B2B technology and IT services trends, including market performance, valuation dynamics, deal activity, and key names to watch

A comprehensive update on B2B technology and IT services trends, including market performance, valuation dynamics, deal activity, and key names to watch

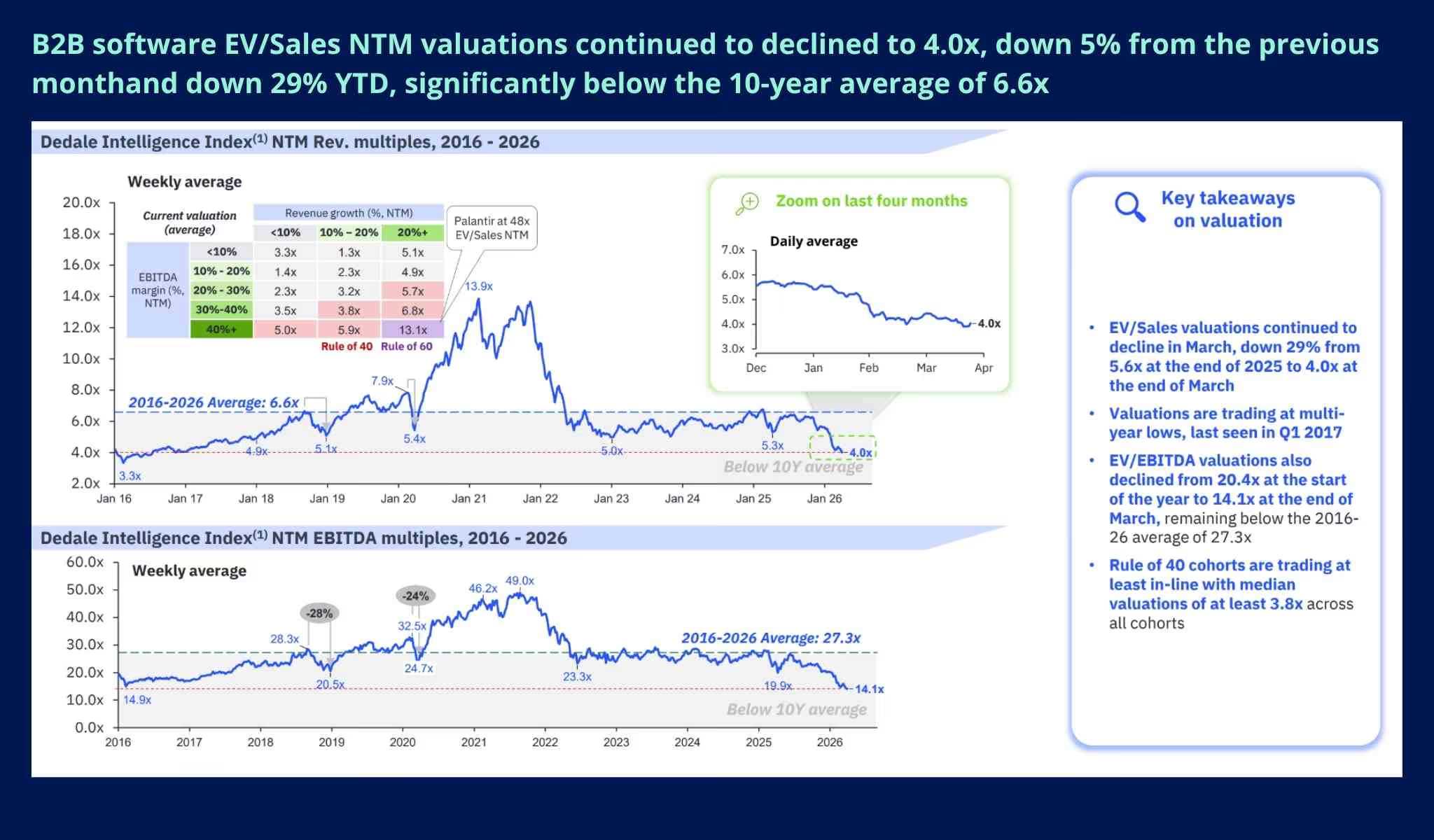

March extended the sustained correction that has defined 2026 for B2B technology equities. The B2B Software Universe fell 4.8% during the month, now down 22.2% year-to-date, a decline that significantly outpaces the broader market and reflects a structural reassessment of software as an asset class.

The sell-off remained broad-based, with all segments posting negative returns year-to-date. Weakness was most pronounced in CRM and Marketing (-31% YTD), Industrial software (-25% YTD), and Majors (-24% YTD), weighed down by sharp declines in Meta (-11.7%), Alphabet (-7.7%), and Microsoft (-5.7%) during the month. The Industrial segment saw the most extreme individual moves, with Cerence (-20.2%), AB Dynamics (-18.0%) and Siemens (-16.9%) among the month's worst performers. On the positive side, Descartes Systems (+10.4%), Samsara (+9.7%) and Tecsys (+9.0%) stood out as rare exceptions.

The correction reflects a deepening investor reassessment of the sector. AI disruption continues to challenge the long-standing perception of software as a structurally high-growth, low-risk asset class, and the market is repricing accordingly.

Valuations compressed further in March, reaching levels not seen since early 2017.

The 10-year average for EV/Sales stands at 6.6x; current multiples have now fallen 40% below that benchmark. The gap between high-growth and low-growth companies remains significant, but all cohorts are under sustained pressure as the market continues to differentiate on forward guidance quality rather than historical growth alone.

Want the full breakdown behind these trends? Download the complete Market Intelligence report to explore detailed data, company-level benchmarks, and deeper analysis across all B2B technology segments.

Deal activity in Q1 2026 painted a polarised picture: venture capital surged in value terms driven by outsized AI financings, while private equity and corporate M&A activity remained cautious.

These dynamics highlight a market in which capital availability is increasingly concentrated, abundant for AI infrastructure plays, disciplined elsewhere.

B2B software listings in March fell below historical averages, with no significant new issuances recorded. Declining SaaS valuations, AI-driven disruption uncertainty, and poor post-IPO performance for recent tech listings continue to suppress appetite. A meaningful recovery in IPO activity is unlikely until public market conditions stabilise and EV/Sales multiples recover to more historically normal levels.

Q4 2025 results showed a sector that remains operationally solid: 18 out of 18 companies tracked reported year-over-year revenue growth, and 16 beat consensus expectations. But market reactions diverged sharply on forward guidance. CrowdStrike was rewarded, posting record net new ARR of $331M (+47% YoY) and Falcon Flex ARR surging 120%+ YoY, while MongoDB sold off approximately 19% post-earnings on weaker FY27 guidance and slowing Atlas growth. The message is clear: delivery alone is no longer enough; the market is pricing future trajectory, not current performance.

This month's deep dive centres on healthcare software, a segment defined by regulatory complexity, fragmented incumbents, and accelerating AI-driven disruption in clinical workflow, diagnostics, and patient management platforms. As with other vertical software categories that hold proprietary data and deep workflow integration, the question is not whether AI will disrupt the segment, but which players are structurally positioned to lead the transition.

Headline CPI inflation stabilised at 2.4% in February 2026, continuing its gradual decline from 2.7% in December. Both the US Federal Reserve and the ECB held rates steady at their most recent meetings. Macro stability provides a floor, but persistent valuation dispersion across software segments suggests the market is not waiting for rate cuts to differentiate, it is already repricing on a company-by-company basis.

Want access to the full Market Update? Download our Market Intelligence report.

Dedale's monthly Market Update provides a curated, data-driven lens into what's really happening in B2B technology, from valuations and macro trends to investment signals and segment-level dynamics.

Want to go deeper on a specific segment, deal, or valuation trend from this month's update? Contact us.

Get started

Dedale is growing fast and we are continuously looking to widen our reach in the ecosystem. Let's connect!

Members

Join our Community of Industry Veterans that we collaborate with to conduct deep research

Join the community

Investors, Corporates, and M&A Advisors

Learn more about how collaborating with Dedale Intelligence could enhance your intelligence generation efforts

Request an introduction

Talents

We are looking for smart, hungry, humble individuals to join our fast growing team worldwide!

Join the team

.jpg)

.jpg)

%20(1).jpg)