B2B Software Market Trends, July 2026: Valuations Dip Again, Supply Chain Software at an Inflection Point

Market Update

B2B Software Market Trends, July 2026: Valuations Dip Again, Supply Chain Software at an Inflection Point

Dedale Intelligence's July 2026 B2B software market update covers valuation dips, supply chain software AI disruption, SpaceX's $80B IPO, Q1 2026 earnings, and deal activity across PE, M&A, and VC.

June reversed the gradual valuation recovery that B2B software had built over April and May. The B2B Software Universe fell 2.4% during the month, while the S&P 500 dropped 1.1% and the Nasdaq fell 2.8%. Year-to-date, the B2B Software Universe is now down 7.0%, significantly lagging the S&P 500, which is up 9.6%, and the Nasdaq, which is up 12.8%.

This update from Dedale Intelligence covers the five themes that shaped B2B software and technology markets in June. For context on where things stood one month prior, see Dedale Intelligence's Market Update June 2026 article & Market Update June 2026 report

Valuations: the recovery stalls

EV/Sales NTM multiples dipped back to 4.3x in June, reversing the gradual recovery seen through April and May. Valuations remain at multi-year lows, last seen in Q1 2017, and continue to trade significantly below the 10-year average of 6.6x. EV/EBITDA valuations followed a similar pattern, falling to 14.9x in June after a partial rebound earlier in the year, remaining well below the 2016 to 2026 average of 27.5x.

The dispersion across segments remains wide. Cybersecurity and Infrastructure Software are the only two segments positive year-to-date, up 30% and 32% YTD respectively, driven by names such as Blackberry (+245.8%), Fortinet (+93.5%), and Mitek Systems (+90.8%) in Cybersecurity, and Rackspace Technologies (+572.6%), DigitalOcean (+226.3%), and OVH Groupe (+97.3%) in Infrastructure Software. All other segments remain negative for the year.

High-growth companies (above 20% NTM revenue growth) trade at 7.5x EV/Sales NTM, versus 3.7x for mid-growth and 2.9x for low-growth cohorts. Rule of 40 companies trade at a premium of 7.6x EV/Sales, while companies below Rule of 20 trade at 2.9x. The premium investors place on revenue growth relative to free cash flow margin has compressed from a peak of 77% in March 2025 to 17% in June 2026. On average, 1% of revenue growth is now valued just 17% more than 1% of FCF margin.

North American software companies trade at 4.9x EV/Sales versus 2.6x for European peers, a premium of 93%, well above the 10-year average premium of 46%.

Source: Dedale Intelligence Analysis

Macro: inflation accelerating, the ECB breaks ranks

Headline CPI rose to 4.2% in May 2026, up from 3.8% in April, continuing the upward trend as energy costs remain the primary driver. Core CPI ticked up slightly to 2.9% from 2.8% in April. The US Federal Reserve held rates steady for a fourth consecutive meeting on June 17, keeping the target range at 3.50% to 3.75%. The ECB broke from its holding pattern and raised rates by 25 basis points on June 11, lifting the deposit facility rate to 2.25%, its first hike since 2023, as eurozone inflation accelerated to 3.2% in May. The move reverses the ECB's prior easing cycle and reflects the same energy-driven inflation pressures that are keeping the Fed from cutting.

Supply chain software: AI adoption accelerates, disruption risk is contained

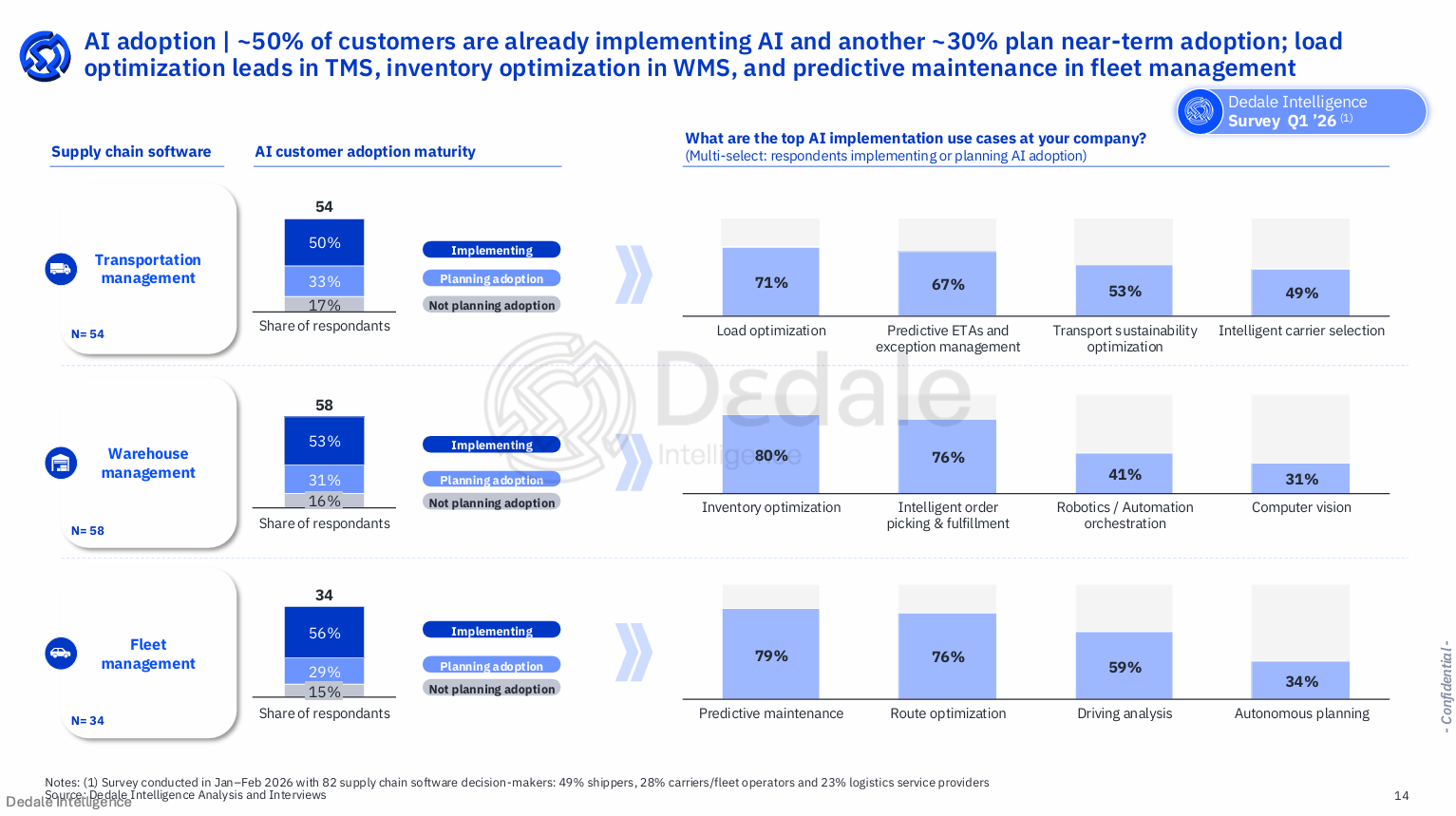

This month's segment deep-dive covers Supply Chain Management software, a market Dedale Intelligence defines across three core execution sub-segments: Transportation Management Software, Warehouse Management Software, and Fleet Management Software.

AI adoption is already a reality for most supply chain software buyers. Across TMS buyers surveyed by Dedale Intelligence in Q1 2026, 50% are already implementing AI and 33% plan near-term adoption. In WMS, 53% are implementing and 31% plan adoption. In Fleet Management, 56% are implementing and 29% plan adoption. The top AI use cases by sub-segment are load optimization and predictive ETAs in TMS; inventory optimization and intelligent order picking in WMS; and predictive maintenance and route optimization in Fleet Management.

Despite this broad AI adoption, Dedale Intelligence's disruption assessment concludes that overall AI disruption risk in supply chain execution software remains limited. WMS, Fleet Management, and TMS are the most protected sub-segments, benefiting from high switching costs, deep workflow integration, and significant proprietary data advantages. Supply Chain Planning and Supply Chain Risk Management face the highest disruption risk, as their solutions are easier to replicate and less deeply embedded in core workflows.

Deal activity in supply chain software remained healthy in 2026, with Q2 showing acceleration driven by platform vendors consolidating AI point solutions. Three key dynamics are shaping the market. Supply chain execution platforms are consolidating through corporate M&A, with platform vendors acquiring AI point solutions to expand horizontally. Private equity exits resumed in 2026, with Riverside exiting Trustwell to TPG and Vontier exiting Teletrac Navman to Respida Capital at a $220M enterprise value, though valuation multiples remain below historical levels. VC and growth funding are focused on agentic AI and physical AI platforms, including Stord's $250M Series F at a $3bn valuation and Mytra's $120M Series C.

Deal activity: corporate M&A surges, AI investment hits $318B YTD

Q2 2026 quarter-to-date deal activity is ahead of Q2 2025 levels across all three segments.

Private equity has reached approximately €6bn across 72 deals. Corporate M&A has surged to approximately €27bn quarter-to-date, driven by GBTG (approximately €5.6bn), Brex (approximately €4bn), and Fin (approximately €3bn). Notable June transactions include Clearwater Analytics taken private by Permira and Warburg Pincus at $8.4bn (a 47% premium to the undisturbed share price), Salesforce's agreement to acquire Fin for approximately $3.6bn, Nuvei's agreement to acquire Payoneer for approximately $2.75bn, and Schneider Electric's agreement to acquire Cognite for $3.1bn. In Cybersecurity, Cyera raised $600M in a Series G at a $12bn post-money valuation. In ERP and HCM, Ramp raised $750M in a Series F at a $43.3bn pre-money valuation.

Venture capital tells the bigger story. Q2 2026 quarter-to-date VC volume has reached approximately €74bn across 1,008 deals, driven by Anthropic's approximately €55bn raise, pushing 2026 YTD VC volume to €232bn. Total 2026 YTD AI investment has already surpassed the full-year 2025 total, reaching $318bn. In June alone, approximately $12.5bn was invested across 119 AI-related deals. Four mega-deals above $500M accounted for approximately 24% of June investment. Excluding mega-deals, the broader AI market recorded approximately $10bn across 115 deals, with June being the highest month on record for investments under $500M since tracking began.

For related context on how the AI investment landscape shaped up the prior month, see Dedale Intelligence's June 2026 Market Trends article.

June 2026 saw 35 IPOs across all sectors, above the long-term average of 32. The total offer amount was dominated by SpaceX's approximately $80bn IPO raise, which alone represents around 60% of the 2026 YTD total offer amount. SpaceX began trading on the New York Stock Exchange under the ticker SPCX on June 12, 2026, priced at $135 per share, valuing the company at approximately $1.77 trillion.

Only one B2B software company went public in 2026 YTD as of June. The broader recent vintage of B2B software IPOs remains mixed in terms of post-debut performance. Among those tracked by Dedale Intelligence, CoreWeave is the standout at +141.5% since its March 2026 IPO. Navan (travel and expense management) is up 14.1% over three months. On the downside, Figma is down 83.9% since its July 2025 IPO following profit-taking after an initial surge of approximately 250%. Via (transit technology) is down 64.7% since IPO. HawkEye360, which listed in May 2026, is down 37.5% since its IPO date.

Q1 2026 Earnings: 11 of 11 beat, only 2 traded up

Dedale Intelligence tracked the remaining 11 companies reporting Q1 2026 results this month. All 11 reported year-over-year revenue growth, all 11 beat consensus expectations, and 9 of 10 raised guidance. Yet only 2 of 11 traded up post-release. The pattern is the same as the prior earnings batch: after the S&P 500 climbed approximately 16% over April and May, expectations were stretched and the market was highly critical on the quality of the beat and the credibility of guidance.

Selected highlights from the cohort:

Oracle fell 4.3% despite total revenue of $19.2bn growing 20.6% year-over-year and beating consensus by 13.5%, with Cloud Infrastructure up 93% to $5.8bn and multicloud database revenue up 404%. The negative reaction reflected full-year free cash flow of negative $23.7bn against heavy AI data-center capital expenditure, despite operating cash flow of $32bn (+54%).

CrowdStrike fell 13.9% on a modest 1.7% revenue beat against elevated expectations, despite net new ARR of $255.8M (+32% year-over-year) lifting ending ARR to $5.51bn (+24%), and a raised FY27 outlook.

Guidewire fell 17.6% on ARR growth of +19% landing only within the guided range alongside a services-heavy mix, despite 11 cloud deals closed and agentic tooling cutting migration timelines by approximately 35%.

Descartes gained 2.5% on services revenue up 15% to $180.5M representing 93% of total revenue, operating income up 35% to $62.5M, and an adjusted EBITDA margin of 46%.

Sprinklr gained 4.8% on improving renewal trends with the $1M-plus customer cohort posting 115% net dollar expansion rate.

The full earnings coverage across all 11 companies, including revenue figures, consensus beats, guidance adjustments, and Dedale Intelligence's segment-level perspective, is in the full report.

Source: Dedale Intelligence Analysis

How Dedale Intelligence tracks B2B software markets

Dedale Intelligence publishes a monthly B2B software Market Session for private equity funds, corporate development teams, and M&A advisors across North America and Europe. The analysis in this article is drawn from the July 2026 Market Session. The full report contains detailed valuation tables by segment and cohort, the complete Supply Chain Software segment deep-dive including the AI disruption matrix and deal-by-deal analysis, the full IPO tracker, earnings coverage across all 11 remaining Q1 2026 companies, and the segment zoom covering financials and valuations across the full B2B software universe. For related analysis on industrial and supply chain software dynamics, see Dedale Intelligence's take on industrial software.

.jpg)

.jpg)

%20(1).jpg)