B2B Software Market Trends, June 2026: Recovery Signals, RegTech Disruption, and a Record AI Raise

Market Update

B2B Software Market Trends, June 2026: Recovery Signals, RegTech Disruption, and a Record AI Raise

Dedale Intelligence's June 2026 B2B software market update covers valuation recovery, RegTech AI disruption, Anthropic's $65B raise, key M&A deals, IPO signals, and Q1 2026 earnings across 33 companies.

May 2026 delivered the clearest recovery signal yet for B2B software valuations. The B2B Software Universe gained 12.9%, outpacing the S&P 500 (up 5.1%) and the Nasdaq (up 8.4%). After months of sustained compression, the question investors are asking is whether this is a genuine floor or a temporary bounce.

Valuations: recovery continues, but context matters

EV/Sales NTM multiples rose to 4.6x by end of May, the third consecutive monthly improvement following the sharp contraction from 5.6x at the start of the year. Current levels remain 18% below January 2026 and significantly below the 10-year average of 6.6x. EV/EBITDA valuations recovered to 16.5x, still well below the long-term average of 27.5x.

The recovery was far from uniform. Cybersecurity led all segments at +34% for the month, driven by Rackspace Technologies (+254.1%), Okta (+67.4%), and Snowflake (+87.3%). Infrastructure Software gained 27%. ERP/HCM and CRM/CMS remain the weakest year-to-date at -27% and -31% respectively.

High-growth companies (above 20% NTM revenue growth) command a premium at 8.3x EV/Sales versus 3.2x for low-growth cohorts. One structural shift worth watching: the premium investors place on revenue growth over free cash flow margin has compressed from a peak of 77% in March 2025 to just 22% in May 2026. The market is demanding both.

North American software companies trade at 5.2x versus 2.8x for European peers, a gap now at 93% versus the 10-year average premium of 46%.

Source: Dedale Intelligence Analysis

Macro: inflation accelerating, rates on hold

Headline CPI surged to 3.8% in April 2026, up from 3.3% in March, driven by energy costs jumping 17.9% year-over-year as the Iran conflict continued to disrupt global supply. Core CPI remained more contained at 2.8%. Both the US Federal Reserve (3.50 to 3.75%) and the ECB (2.00%) held rates unchanged at their most recent meetings. Three consecutive holds from the Fed signal that the easing cycle is effectively paused, with officials flagging the possibility of rate hikes if energy-driven price pressures persist.

RegTech: AI moves from experimentation to institutionalization

This month's segment deep-dive covers AI-native Financial Crime software spanning KYC, AML, and identity verification. The central finding from Dedale Intelligence's research: 75% of financial institutions surveyed are already using or piloting AI in their compliance stacks. AI is becoming a baseline expectation in product roadmaps, not a differentiator.

Three dynamics define the current deal market. VC capital is flowing into AI-native challengers at Series A and B stage, with Feedzai's $75m Series E at a $2bn valuation confirming that late-stage AI-native FinCrime can scale. Tier-1 vendors are choosing partnerships over acquisition to close capability gaps, most notably FIS partnering with Anthropic to embed agentic AML investigations into core banking, compressing alert review from hours to minutes. PE consolidation has reopened at the top of the market, anchored by NICE Actimize's approximately $2.5bn sale process with five bidders advancing to Phase 2 due diligence.

The full RegTech analysis including Dedale Intelligence's AI opportunity matrix, complete survey findings, and exit window analysis across five FinCrime platforms in hold periods is in the full report: Download the full June 2026 Market Intelligence report

Q2 2026 quarter-to-date deal activity is ahead of Q2 2025 levels across all three segments.

Private equity has reached approximately €6bn across 45 deals. Corporate M&A has rebounded to approximately €18bn versus approximately €4bn in Q1 2026, lifted by Autodesk's acquisition of MaintainX (approximately €3bn, at approximately 26 to 27x ARR), the Forsta transaction (approximately €5.7bn), Sierra's $950m Series E at a valuation exceeding $15bn, and Publicis Groupe's $2.2bn acquisition of LiveRamp at a 29.8% premium.

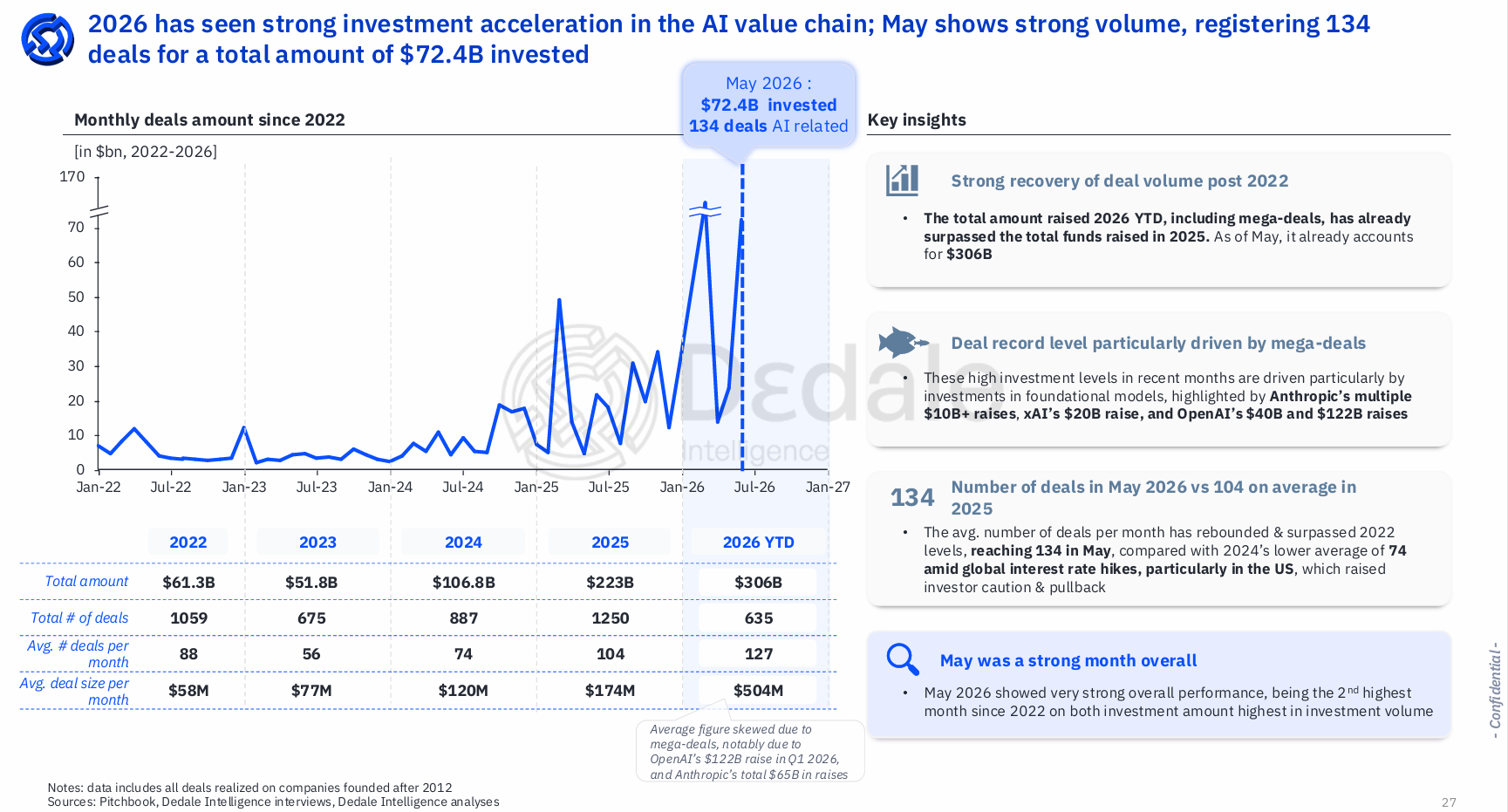

Venture capital tells the biggest story. Q2 2026 quarter-to-date VC volume has surged to approximately €66bn across 626 deals, driven by Anthropic's approximately €55bn raise. That is the $65bn Series H closed at a $965bn post-money valuation, co-led by Altimeter Capital, Dragoneer, Greenoaks, and Sequoia Capital. 2026 YTD AI investment has now reached $306bn, a 153% jump versus full-year 2025 in just five months.

May alone saw $72.4bn invested across 134 AI-related deals, the second highest month since 2022. Eleven mega-deals accounted for 89% of that total. Excluding deals above $500m, the broader market recorded $8bn across 123 deals, confirming AI investment is broadening well beyond foundational model mega-rounds.

For more on Anthropic's competitive position and what this funding means for the foundational model market, see Dedale Intelligence's Anthropic Private Market Leader 360.

Source: Dedale Intelligence Analysis

IPOs: a window cracks open

May 2026 saw 41 IPOs across all sectors, above the long-term average of 32. The one notable B2B software listing was HawkEye360, a geospatial analytics platform converting radio frequency signals into actionable intelligence for defense, government, and commercial clients. It raised $416m and listed on the NYSE under the ticker HAWK at $26 per share (approximately $2.4bn valuation), ending the month down 25.9% from its IPO price.

The broader recent vintage of B2B software IPOs remains largely underwater. Of the cohort tracked by Dedale Intelligence, only CoreWeave (+151%) has delivered meaningful post-listing returns. The IPO window for B2B software is cracked, not open.

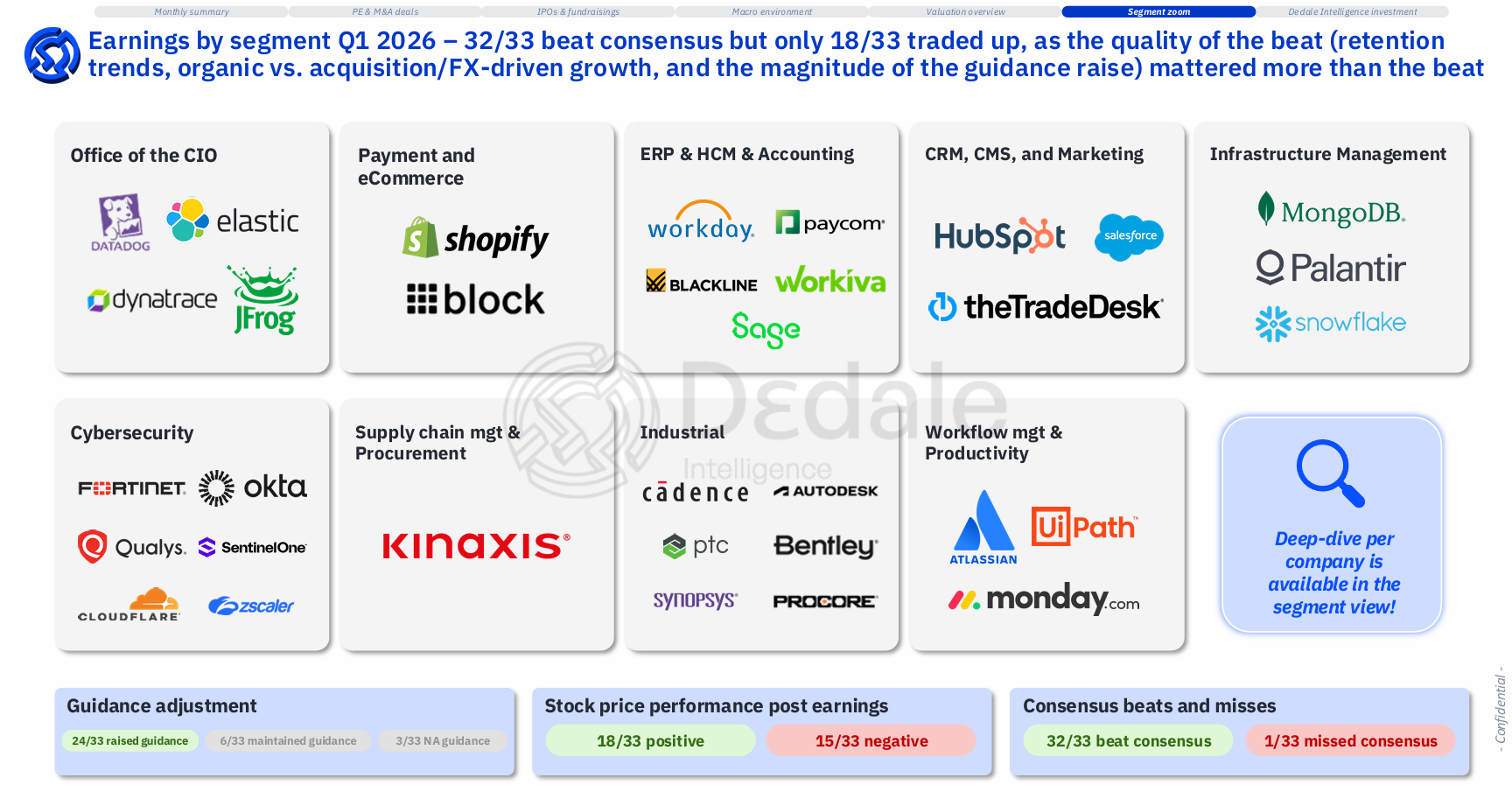

Q1 2026 Earnings: strong beats, divided reactions

Dedale Intelligence tracked 33 companies reporting Q1 2026 results. All 33 reported year-over-year revenue growth, 32 of 33 beat consensus, and 24 of 33 raised guidance. Yet stock reactions split almost evenly with 18 up and 15 down. The market priced the quality of the beat, not just the fact of it. Retention trends, organic versus acquisition-driven growth, and the magnitude of the guidance raise mattered more than the headline number.

Snowflake led all companies with a +59.8% stock reaction on net revenue retention rising to 126%, RPO up 38% to $9.21bn, and 779 $1M-plus customers. Atlassian gained 35.8% on cloud growth reaccelerating to 29%. In direct contrast, Cloudflare fell 27.3% despite 33.5% revenue growth, as a surprise restructuring charge and gross margin compression to 72.8% overshadowed the beat entirely.

HubSpot fell 26.1% despite raising guidance because net revenue retention slipped to 103%. Palantir fell 6.1% despite a Rule of 40 of 145% and 206 deals above $1M, because the stretched multiple left no room for anything short of a blowout raise.

The full earnings coverage across all 33 companies with detailed highlights, guidance changes, and Dedale's segment-level perspective is in the full report.

Source: Dedale Intelligence Analysis

How Dedale Intelligence tracks B2B software markets

Dedale Intelligence publishes a monthly B2B software Market Session for private equity funds, corporate development teams, and M&A advisors across North America and Europe. The analysis in this article is drawn from the June 2026 Market Session. The full report contains detailed valuation tables, the complete RegTech deep-dive, deal-by-deal analysis, and earnings coverage across all 33 companies.

.jpg)

.jpg)